SMALL BUSINESS CGT CONCESSIONS: WHEN DO I QUALIFY?

The small business CGT concessions are a great tool for business owners to transfer wealth into super. Here, we break down the two essential requirements you must first meet in order to access any of the concessions. Could your business qualify? It may be time to see your adviser to start planning your business retirement strategy.

Have you considered the powerful tax and superannuation planning opportunities that the small business CGT concessions can offer your business? These concessions allow you to reduce – or in some cases, completely eliminate – the capital gain from the sale of a business asset, whether it’s held directly by your business entity or in another related structure.

Read More

AUSTRALIA'S THREE-PILLAR RETIREMENT INCOME SYSTEM

Depending on your personal circumstances, your retirement incomemay come from a variety of sources. For example, investments (inside and/or outside super) and social security entitlements, such as the Age Pension.

These sources of retirement income are important to understand; especially if, for example, you envision yourself enjoying a particular type of lifestyle in retirement.

Read More

DEBT FORGIVENESS DUE TO LOVE AND AFFECTION

The rules around Div 7A deemed dividends are complex and may have become more so with the release of a draft taxation determination from the ATO in relation to debts forgiven. Contrary to previous guidance, the draft determination now indicates only natural persons can forgive debts by reasons of natural love and affection. Therefore, private companies will no longer be able to use this exemption on debts forgiven. If your private company has previously used this exemption, beware as the Tax Office has indicated that it will apply this new view in any litigation matters.

Private companies that pay amounts of money, make loans, or forgives debts of shareholders or associates of shareholders, may be subject to Div 7A rules which are designed to ensure that income is not inappropriately sheltered at the corporate tax rate. Generally, these rules deem certain moneys and/or benefits (eg loans and forgiven debts) obtained from the private company by shareholders or their associates to be dividends.

Read More

CROWDFUNDING: IS IT INCOME?

Crowdfunding has fast become the go to place for people in need of large amounts of money quickly, but is the money raised considered to be income and therefore taxable? Campaigns on various platforms range from the shameless (lavish weddings/honeymoons) to ground-breaking (new innovative products), and whether each campaign is taxable depends entirely on the circumstances of each case. Generally, if the campaign is related to running/furthering your business or is a profit-making plan, then any money received would be classed as income.

These days it feels like everything is being crowdfunded, you may have heard the ridiculous story of a man who wanted to raise US$10 for a potato salad and ended up with US$55,000 from complete strangers. Or perhaps you’ve heard stories of shameless couples who wanted to people to fund their lavish weddings or honeymoons? Crowdfunding has fast become the go to place for people in need of large amounts of money quickly, but is the money raised taxable?

Read More

BEWARE OF INSURANCE CHANGES IN SUPERANNUATION

You may have heard a lot recently about super funds providing either opt-in or opt-out insurance and have wondered how will affect you and your retirement savings. Perhaps you’ve heard horror stories about super funds cancelling people’s insurance. Don’t fret, in most cases cancellation of insurance only happens in limited instances, and your fund will most likely notify you before any cancellation occurs. As for opt-in and opt-out insurance, the changes are coming, but not until 1 April 2020, so if you’re affected you’ll have plenty of time to prepare.

Insurance within superannuation has always been a mixed blessing, good for some who enjoy having cheaper insurance, while others see as an erosion of their super balances. It doesn’t matter which camp you fall into, the recent changes to the way super funds provide insurance may impact you depending on your super balance, age, and when your last contribution was.

Read More

GENUINE REDUNDANCY PAYMENT: AGE INCREASE

The qualifying age to receive a genuine redundancy payment has recently been increased to the age pension age, so even if you’re over 65 you may still be able to receive the payment. The advantage of that is you’ll potentially be able to work longer and retire later in life whilst still being able to receive a tax-free genuine redundancy payment. However, the rules surrounding this area is quite complex and is largely dependent on the facts of each case, so caution is advised.

With everyone retiring later in life and working longer, the government has been playing catch up to align some outdated age provisions in the tax law to today’s standards. One such change brings into line the genuine redundancy payment’s qualifying age with the age pension age. In real world terms, it means the qualifying age has been increased from 65 to between 66 or 67 depending on the year you were born. So, if you’re dismissed on or after 1 July 2019, and are between 65 and 67, you may potentially qualify for more of your redundancy payment to be tax-free depending certain eligibility conditions.

Read More

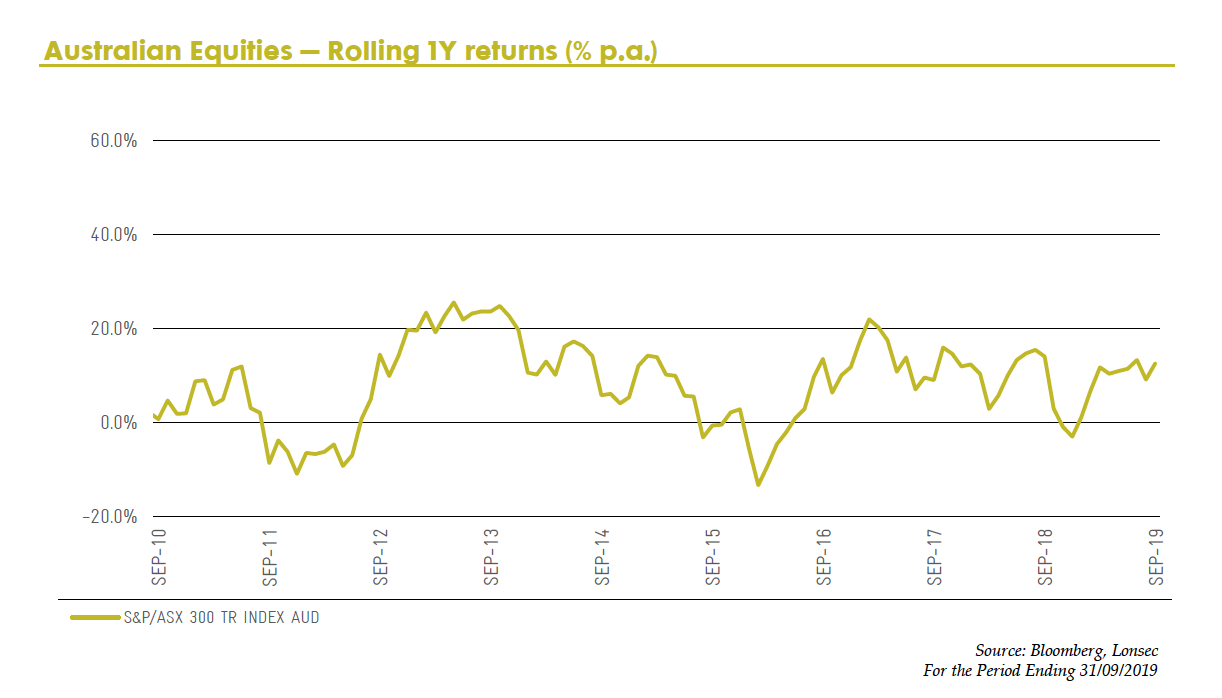

OCTOBER REPORT

Australian shares managed to reclaim some ground in September which saw the S&P/ASX 200 Index post a modest 1.8% return before falling in the first week of October. Energy was the top performing sector, returning 4.7% and clawing back some losses from the previous month. Oil price spiked in September, the result of major disruption to the oil market, which favoured energy producers like Santos (+7.2%) and Beach Energy (+3.3%). The financial services sector (+4.1%) saw broad growth over the month. Shares in IOOF (+26.0%) rose as the wealth manager completed its sale of Ord Minnett during the month and the Federal Court dismissed a case brought against it by APRA that accused executives of failing to act in its members’ interests.

Read More

SELLING SHARES: HOW DOES TAX APPLY?

Did you know that when you sell your shares, the size of your capital gains tax bill is affected by how long you’ve held the shares, and how you offset your capital gains and losses? Knowing the tax rules can help you plan ahead. Whether you own just a few listed shares or have an extensive portfolio, understanding how capital gains tax (CGT) applies when you sell your shares can help you plan your trades effectively. Here, we break down the rules for taxpayers who hold their shares as a passive investment. If you trade shares on a scale that amounts to a business of share trading, talk to your tax adviser about the different tax regime that applies. Each time you sell a parcel of shares, you trigger a “CGT event” and you must work out whether you’ve made a capital gain on that parcel (where the proceeds you receive exceed the cost base) or capital loss (where the cost base exceeds the proceeds). You also trigger a CGT event if you give the shares away as a gift – perhaps to a family member. For tax purposes, you’re deemed to have disposed of the shares at their full market value.

Read More

CLOSING THE TAX GAP: ATO FOCUS ON INDIVIDUAL RETURNS

The ATO will scrutinise every individual tax return lodged for the 2018-19 income year to find instances of incorrect claims. It is encouraging taxpayers to document supporting evidence for all claims as it seeks to recoup $8.7bn in lost tax revenue each year from small over-claims by a large proportion of taxpayers. Red flags which may lead to ATO contact or audit include under reported income (from third party data) and deductions that appear high compared to others with a similar job and income level.

As this year’s tax time comes to a close, the ATO has warned that it will scrutinise every individual tax return lodged to seek out incorrect claims. In particular, it will be on the lookout for under reported income as indicated by third party data, and deductions that appear high compared to people with a similar job and income level.

Read More