OCTOBER REPORT

Australian shares managed to reclaim some ground in September which saw the S&P/ASX 200 Index post a modest 1.8% return before falling in the first week of October. Energy was the top performing sector, returning 4.7% and clawing back some losses from the previous month. Oil price spiked in September, the result of major disruption to the oil market, which favoured energy producers like Santos (+7.2%) and Beach Energy (+3.3%). The financial services sector (+4.1%) saw broad growth over the month. Shares in IOOF (+26.0%) rose as the wealth manager completed its sale of Ord Minnett during the month and the Federal Court dismissed a case brought against it by APRA that accused executives of failing to act in its members’ interests.

The materials sector (+3.1%) also saw significant gains for some members, led by Western Areas (+25.0%), which benefitted from a rise in the Nickel price after the Indonesian government announced a ban on exports of raw ore. Nufarm shares (+17.0%) shot higher following the announcement that it was selling its South American business to Japanese conglomerate Sumitomo. Large cap shares rose 2.0% with solid gains from major banks and miners, but were outshone by their small cap peers, which returned 2.6%.

Global markets adjusted to renewed geopolitical risks, including the US-China trade dispute, growing tensions in the Middle East, the threat of impeachment, protests in Hong Kong, and the ongoing Brexit saga. A drone attack on a major Saudi Arabian oil facility, which

wiped out 5.7 million barrels of production per day, or around five percent of the world’s supply, wrought havoc on oil markets. Economic indicators point to a rise in the risk of a US recession and a possible turning point in equities, but so far markets appear satisfied with the low rate of US unemployment, and the bullish trend since the start of 2019 remains intact.

Developed market shares outside Australia rose 1.8% in Australian dollar terms as investors tentatively re-entered equities following selling in the previous month. In the US, energy shares (+3.6%) were boosted by the spike in oil prices. Marathon Petroleum (+23.5%) jumped higher, but this wasn’t enough to placate major shareholders disappointed with its recent under-performance. European shares had a positive month, with the STOXX Europe 600 Index rising 3.6%, led by financial services, auto and energy sectors. In Asian markets, China’s CSI 300 Index was mostly flat at 0.5%, Hong Kong’s Hang Seng Index rose 1.9%, and Japan’s Nikkei 225 Index rose 5.9%.

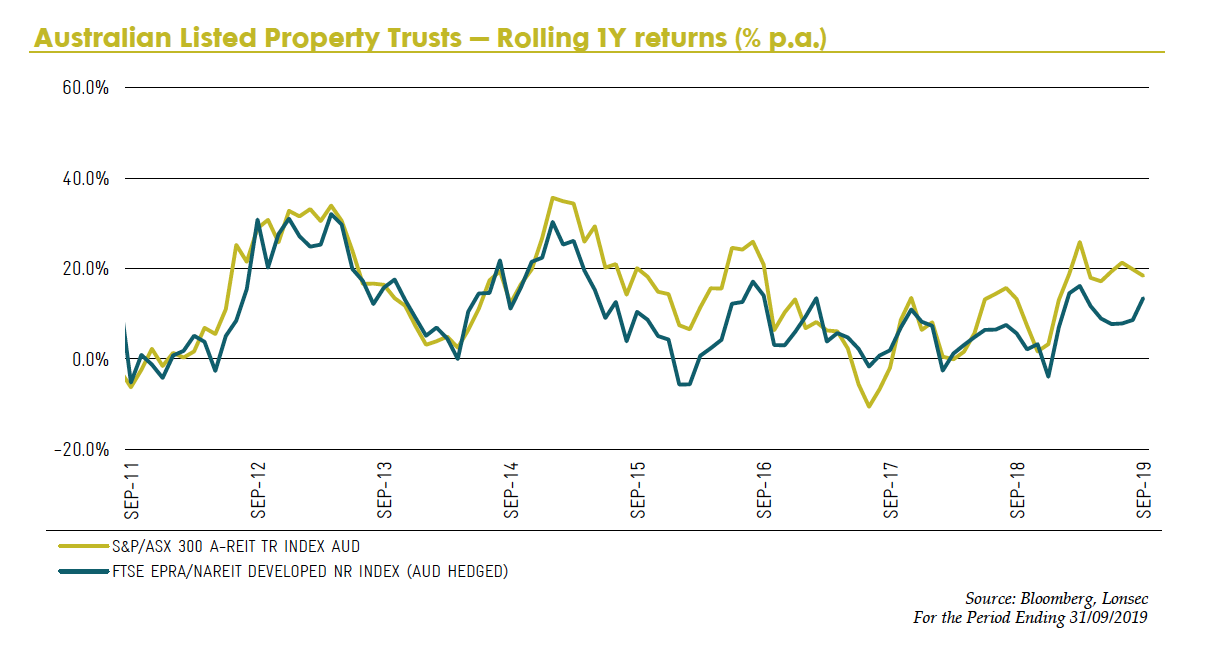

September was a trying month for listed property as the S&P/ASX 200 A-REIT Index lost 2.7% as a temporary rise in yields undermined values, but the broad low-rate environment is likely a positive for property as investors continue their hunt for yield. Commercial managers Charter Hall Group (-7.9%) and Dexus (-7.5%) experienced the largest drops over the month, while retail and shopping centres also struggled. The improvement in house prices since June may now be flowing through to an improvement in housing finance.

However, from an activity perspective, what is important is the trajectory of dwelling construction and the associated flow-on to retail spending on household goods and furnishings. It is difficult to envisage a recovery in housing construction any time soon given supply issues and the projection of ongoing subdued wages growth. While credit to housing has improved, credit to developers and businesses is appears to be affected by the royal commission. Globally, REITs had a positive month in September, rising 3.0% in developed markets. US REITs were positive in September, returning 1.5% in US dollar terms, with gains from shopping centres (+8.4%), regional malls (+5.6%) and hotels (+5.2%).

While equities were choppy, it was the bond market that revealed the full extent of investor indecisiveness. September began with a sharp sell-off in bonds as markets, which may have been partly due to high-than-expected US inflation, along with evidence of robust consumer spending. The US 10-year Treasury yield jumped from 1.50% at the start of the month to 1.90% on 13 September, before falling back down to just over 1.50% in early October. The result was a capital loss on 10-year bonds of around 3% over a 10-day period, making the pace and magnitude of the sell-off among the most severe.

Over the course of September, global bonds, measured by the Bloomberg Barclays Global Aggregate Index, fell 0.6% in Australian dollar hedged terms, while Australian bonds fell 0.5%. The 10-year minus 3-month portion of the yield curve has been inverted since May, raising concerns for some Fed members. While not the only indicator on the ‘recession dashboard’, at the very least it indicates that investors are nervous about future growth. It could also be a sign that Fed policy is too tight and that rates need to be reduced further. September also saw a spike in the overnight lending rate between US banks, which jumped to levels not seen since 2008, prompting cash injections from the Fed to support liquidity.

Are markets expensive or inexpensive?

One of the topics asset allocators are grappling with at the moment is whether asset class valuations are expensive or not. Whether you’re an active asset allocator or an active bottom-up stock picker, valuation will most likely form the core or at least a significant part of your analysis when making a decision to enter or exit an investment. Valuation historically has been a good long-term metric in assessing the potential future return of an asset. However, with interest rates at depressed levels, asset prices which appear expensive based on historical levels don’t appear that expensive given the low interest rate environment.

Equity markets in general, and in particular growth companies expected to grow their free cashflow in the future, have benefited from the low interest rate environment as they tend to be more sensitive to interest rates, similar to a long duration bond. It could be argued that if interest rates remain at low levels (and possibly lower) risk assets will continue to benefit. Despite this we believe that at some point markets will focus on fundamentals and the market will need to demonstrate earnings growth to sustain valuations. Furthermore, studies suggest that the relationship between interest rates and valuations is not linear, meaning that markets benefit from low interest rates to a point.

From an asset allocation perspective, valuation remains an important tool to help make active asset allocation decisions. We believe that in the current environment you also need to consider medium-term signals such as where we are in the cycle, levels of liquidity, and market sentiment, as these factors can influence the extent to which asset prices can remain elevated or depressed for periods of time.

Key Economic and Market Risks

• Return to solid global growth with modest inflation

Positive: Current concerns over a slowdown in economic growth turn out to be overblown. China stabilises growth around 6.0 to 6.5% while US growth holds well above trend. Europe and Japan improve after a weak 2018, supported by extremely easy policies. Emerging market economies recover. Bond yields remain relatively low as inflation remains contained. Equities resume their rally. Positive for cyclical exposures.

• US Fed tightens more than expected

Negative: With US growth slowing, partly as a result of the uncertainty over trade, the Fed is expected to ease policy. However, member concerns about labour market tightness and inflation, along with a desire to avoid being seen as caving to political pressure, means the Fed refrains, at least initially. Markets weaken.

• European political risks intensify

Negative: The rise of populist parties across Europe leads to policies aimed at reducing immigration and backtracking on globalisation. Recent developments in Italy are a case in point, with a rise in the fiscal deficit adding to already high debt levels, raising the risk of further rating downgrades and concern over the euro. The prospect of a hard Brexit and the resulting economic dislocation causes markets to panic. Equity markets suffer and defensive assets outperform.

• Global geopolitical risks intensify

Negative: Responses from US trade partners over tariff rises results in a trade war and protectionist policies as the new political norm. While the two Koreas appear to have defused tensions for now, there is still a risk that the situation could become inflamed, while uncertainty over the position of other major powers undermines risk appetite and markets.

• US and China fail to reach a trade deal

Negative: Failed trade negotiations between the US and China lead to a prolonged trade war and an escalation in tensions. This leads to lower growth as real consumption declines and heightened uncertainty undermines investment. Financial markets experience weakness and volatility, adding to the weaker outlook.

• Chinese “hard landing”

Negative: The Chinese authorities are slow and too timid in their response to the current cyclical and structural downturn given their increased emphasis on financial stability. This causes a sharp downturn in the property market, exposing high levels of local government debt and undermines consumer spending. The yuan is allowed to depreciate and capital outflows intensify. This leads to GDP growth well below 5.0%. Negative for the global economy but also the Australian economy, equities, commodity prices, emerging markets and particularly resources and the Australian dollar. Bonds outperform.

• Low interest rates, tax cuts, and stronger commodities

Positive: With cash and mortgage rates at, or near, record lows, the currency at reasonable levels, and a sharp improvement in the fiscal position allowing for tax cuts, the domestic economy surprises to the upside. This, along with a renewed lift in global growth and commodity prices, and strengthening infrastructure investment, flows through to domestic employment, incomes and growth. Domestic equities lift. RBA signals eventual tightening.

• Australian house prices continue to weaken

Negative: Despite rate cuts, fiscal easing and easier lending conditions, weaker global growth exposes Australia’s imbalances and high debt levels. Households continue to roll back spending in the face of rising unemployment, low wages growth and uncertainty, but this time there are no sectors coming to rescue the domestic economy. Investment turns down, any housing recovery is aborted, and the government is slow to ease fiscal policy. The bank sector is impacted. The Australian dollar weakens and equities and bond yields move lower

IMPORTANT NOTICE: This document is published by Lonsec Research Pty Ltd ABN 11 151 658 561, AFSL No. 421445 (Lonsec). Please read the following before making any investment decision about any financial product mentioned in this document. Disclosure at the date of publication: Lonsec receives a fee from relevant fund manager or product issuer(s) for researching financial products (using comprehensive and objective criteria) which may be referred to in this Report. Lonsec may also receive a fee from the fund manager or product issuer(s) for subscribing to research content and other Lonsec services. Lonsec receives fees for providing investment consulting advice to clients, which includes model portfolios, approved product lists and other financial advice. Lonsec’s fees are not linked to the financial product rating(s) outcome or the inclusion of the financial product(s) in model portfolios, or in approved product lists. Lonsec may hold any financial product(s) referred to in this document. Lonsec’s representatives and/or their associates may hold any financial product(s) referred to in this document, but details of these holdings are not known to the analyst(s). Warnings: Past performance is not a reliable indicator of future performance. Any express or implied rating or advice presented in this document is a “class service” (as defined in the Financial Advisers Act 2008(NZ)) or limited to “general advice” (as defined in the Corporations Act 2001(Cth) and based solely on consideration of the investment merits of the financial product(s) alone, without taking into account the investment objectives, financial situation and particular needs (“financial circumstances”) of any particular person. Before making an investment decision based on the rating or advice, the reader must consider whether it is personally appropriate in light of his or her financial circumstances or should seek independent financial advice on its appropriateness. If our financial advice relates to the acquisition or possible acquisition of a particular financial product, the reader should obtain and consider the Investment Statement or the Product Disclosure Statement for each financial product before making any decision about whether to acquire the financial product. Disclaimer: Lonsec provides this document for the exclusive use of its subscribers. It is not intended for use by a retail client or a member of the public and should not be used or relied upon by any other person. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document, which is drawn from public information not verified by Lonsec. Financial conclusions, ratings and advice are reasonably held at the time of completion (refer to the date of this report) but subject to change without notice. Lonsec assumes no obligation to update this document following publication. Except for any liability which cannot be excluded, Lonsec, its directors, officers, employees and agents disclaim all liability for any error or inaccuracy in, misstatement or omission from, this document or any loss or damage suffered by the reader or any other person as a consequence of relying upon it. Copyright © 2015 Lonsec Research Pty Ltd (ABN 11 151 658 561, AFSL No. 421445) (Lonsec). This report is subject to copyright of Lonsec. Except for the temporary copy held in a computer's cache and a single permanent copy for your personal reference or other than as permitted under the Copyright Act 1968 (Cth), no part of this report may, in any form or by any means (electronic, mechanical, micro-copying, photocopying, recording or otherwise), be reproduced, stored or transmitted without the prior written permission of Lonsec. This report may also contain third party supplied material that is subject to copyright. Any such material is the intellectual property of that third party or its content providers. The same restrictions applying above to Lonsec copyrighted material, applies to such third party content.