2022/23 Federal Budget

Personal income tax changes

Increase to low and middle income tax offset (‘LMITO’)

The Government has announced a once-off $420 ‘cost of living tax offset’ for the 2022 income year, which will be provided in the form of an increase to the existing LMITO. This will increase the maximum LMITO benefit to $1,500 for individuals and $3,000 for couples, and will be paid from 1 July 2022 when Australians submit their tax returns for the 2022 income year.

Other than those who do not require the full offset to reduce their tax liability to zero, all LMITO recipients will benefit from the full $420 increase. All other features of the LMITO remain unchanged.

To the extent an individual is entitled to an amount of LMITO for the 2022 income year under the current law, their entitlement is proposed to be increased by $420, as follows:

The LMITO is not available from the 2023 income year.

Increasing the Medicare levy low-income thresholds

The Government will increase the Medicare levy low-income thresholds for seniors and pensioners, families and singles from 1 July 2021 as follows:

• The threshold for singles will be increased from $23,226 to $23,365.

• The family threshold will be increased from $39,167 to $39,402.

• For single seniors and pensioners, the threshold will be increased from $36,705 to $36,925.

• The family threshold for seniors and pensioners will be increased from $51,094 to $51,401. For each dependent child or student, the family income thresholds will increase by a further

$3,619 instead of the previous amount of $3,597.

Tax deductibility of COVID-19 test expenses

The Government will ensure that the costs of taking a COVID-19 test to attend a place of work are tax deductible for individuals from 1 July 2021. In making these costs tax deductible, the Government will also ensure FBT will not be incurred by businesses where COVID-19 tests are provided to employees for this purpose.

Changes affecting business taxpayers

Skills and training boost

The Government will introduce a skills and training boost to support small and medium-sized businesses to train and upskill their employees. The boost will apply to eligible expenditure incurred from 7:30pm (AEDT) on 29 March 2022 (i.e., Budget night) until 30 June 2024.

Small and medium-sized businesses (with aggregated annual turnover of less than $50 million) will be able to deduct an additional 20% of expenditure incurred on external training courses provided to their employees. The external training courses will need to be provided to employees in Australia or online and delivered by entities registered in Australia.

Some exclusions will apply, such as for in-house or on-the-job training and expenditure on external training courses for persons other than employees.

For eligible expenditure incurred by 30 June 2022, the boost will be claimed in tax returns for the following income year. For eligible expenditure incurred between 1 July 2022 and 30 June 2024, the boost will be claimed in the income year in which the expenditure is incurred.

Technology investment boost

The Government will introduce a technology investment boost to support digital adoption by small and medium-sized businesses. The boost will apply to eligible expenditure incurred from 7:30pm (AEDT) on 29 March 2022 (i.e., Budget night) until 30 June 2023.

Small and medium-sized businesses (with aggregated annual turnover of less than $50 million) will be able to deduct an additional 20% of expenditure incurred on business expenses and depreciating assets that support their digital adoption (such as portable payment devices, cyber security systems or subscriptions to cloud-based services).

An annual cap will apply in each qualifying income year so that expenditure up to $100,000 will be eligible for the boost. This equates to a maximum additional deduction of $20,000 per eligible year.

For eligible expenditure incurred by 30 June 2022, the boost will be claimed in tax returns for the following income year. For eligible expenditure incurred between 1 July 2022 and 30 June 2023, the boost will be claimed in the income year in which the expenditure is incurred.

Modernising the PAYG instalment system

The Government will enable companies to choose to have their PAYG instalments calculated based on current financial performance, extracted from business accounting software, with some tax adjustments. This will support business cash flow by ensuring instalments reflect current performance.

Subject to advice from software providers about their capacity to deliver, it is anticipated that systems will be in place by 31 December 2023, with the measure to commence on 1 January 2024, for application to periods starting on or after that date.

Making COVID-19 business grants non-assessable non- exempt

The Government has extended the measures that enable payments from certain state and territory COVID-19 business support programs to be made non-assessable non-exempt income (‘NANE’) for income tax purposes until 30 June 2022. This measure was originally announced on 13 September 2020.

The Government has made the following state and territory grant programs eligible for this treatment since the 2021-22 Mid-Year Economic and Fiscal Outlook:

• New South Wales Accommodation and Support Grant.

• New South Wales Commercial Landlord Hardship Grant.

• New South Wales Performing Arts Relaunch Package.

• New South Wales Festival Relaunch Package.

• New South Wales 2022 Small Business Support Program.

• Queensland 2021 COVID-19 Business Support Grant.

• South Australia COVID-19 Tourism and Hospitality Support Grant.

• South Australia COVID-19 Business Hardship Grant.

Sharing of Single Touch Payroll (‘STP’) data

The Government has committed to the development of IT infrastructure required to allow the ATO to share STP data with State and Territory Revenue Offices on an ongoing basis.

Funding for this measure has already been provided and will be deployed following consideration of which States and Territories are able, and willing, to make investments in their own systems and administrative processes to pre-fill payroll tax returns with STP data.

Small Business Support Package

The Government will provide funding over three years from 2021/22 to deliver initiatives to support small businesses, including:

• $10.4 million over two years from 2022/23 to enhance and redesign the Payment Times Reporting Portal and Register to improve efficiency and reporting;

• $8.0 million in 2022/23 to the Australian Small Business and Family Enterprise Ombudsman to work with service providers to enhance small business financial capability;

• $4.6 million over two years from 2021/22 to support the New Access for Small Business Owners program delivered by Beyond Blue to continue to provide free, accessible, and tailored mental health support to small business owners; and

• $2.1 million over two years from 2021/22 to extend the Small Business Debt Helpline program operated by Financial Counselling Australia to continue to provide financial counselling to small businesses facing financial issues.

Other budget announcements

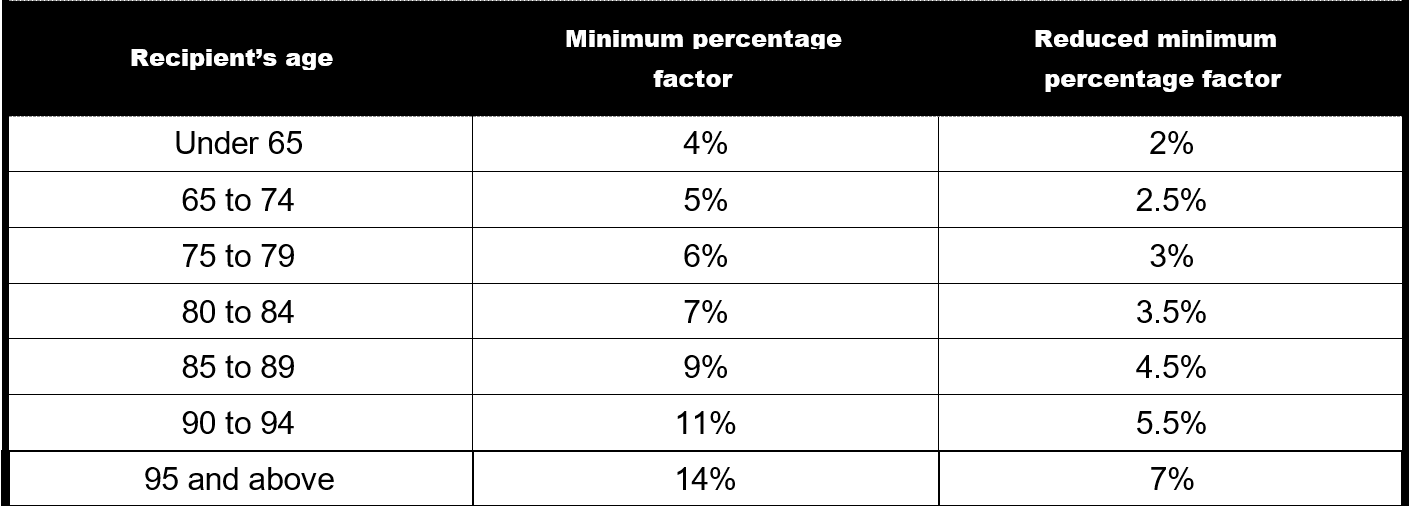

Extending the reduction in minimum drawdowns The Government will extend the 50% reduction of superannuation minimum drawdown requirements for account-based pensions (‘ABPs’) and similar products for a further year to 30 June 2023 (i.e., for the 2023 income year).

Based on this change, the (effective) reduced minimum percentage factors for ABPs (including TRISs), which are used to calculate the minimum annual pension amount under Schedule 7 to the SIS Regulations, are set out in the following table for the 2023 income year.

Note that, for ABPs and TRISs that commence or cease part-way through the 2023 income year, a pro-rated minimum pension payment applies (unless the pension commenced on or after 1 June 2023, in which case, no minimum pension payment is required).

Varying the GDP uplift factor for tax instalments

The Government has decided to set the GDP uplift factor for PAYG and GST instalments at 2% for the 2023 income year. This uplift factor is lower than the 10% that would have applied under the statutory formula.

The lower uplift rate will provide cash flow support to small businesses, including sole traders and other individuals with investment income.

The 2% GDP uplift rate will apply to small to medium enterprises eligible to use the relevant instalment methods (i.e., up to $10 million annual aggregated turnover for GST instalments and $50 million annual aggregated turnover for PAYG instalments) in respect of instalments that relate to the 2023 income year and fall due after the enabling legislation receives Royal Assent.

Digitalising trust income reporting and processing

The Government will digitise trust and beneficiary income reporting and processing by allowing all trust return filers the option to lodge income tax returns electronically, increasing pre-filling and automating ATO assurance processes.

This measure acknowledges that trust income reporting has not been automated to the same extent as individual and company tax returns. This measure will reduce the compliance burden, reduce processing times, and enhance ATO processes.

This measure is proposed to commence from 1 July 2024, subject to advice from software providers about their capacity to deliver.

Expanding access to employee share schemes

The Government will expand access to employee share schemes and further reduce red tape so that employees of all levels can directly share in the business growth they help to generate.

Where employers make larger offers in connection with employee share schemes in unlisted companies, participants can invest up to the following amounts (thereby allowing employers to access simplified disclosure requirements and exemptions from licensing):

• $30,000 per participant per year (which is an increase from $5,000), accruable for unexercised options for up to five years, plus 70% of dividend and cash bonuses; or

• any amount, if it would allow them to immediately take advantage of a planned sale or listing of the company to sell their purchased interests at a profit.

The Government will also remove regulatory requirements for offers to independent contractors, where they do not have to pay for their interests.

Cost of living payment

The Government will provide a one-off $250 cost of living payment to help eligible recipients with higher cost of living pressures. The payment will be made in April 2022 to eligible recipients of the following payments and to concession cardholders:

• Age Pension.

• Disability Support Pension.

• Parenting Payment.

• Carer Payment.

• Carer Allowance (if not in receipt of a primary income support payment).

• Jobseeker Payment.

• Youth Allowance.

• Austudy and Abstudy Living Allowance.

• Double Orphan Pension.

• Special Benefit.

• Farm Household Allowance.

• Pensioner Concession Card holders.

• Commonwealth Seniors Health Card holders.

• Eligible Veterans’ Affairs payment recipients and Veteran Gold cardholders.

The payments are exempt from tax and will not count as income support for the purposes of any income support payment. A person can only receive one economic support payment, even if they are eligible under two or more categories outlined above.

The payment will only be available to Australian residents.

Temporary reduction in fuel excise

The Government will help reduce the burden of higher fuel prices by halving the excise and excise- equivalent customs duty rate that applies to petrol and diesel, and all other fuel and petroleum- based products except aviation fuels, for six months. This measure will commence from 12.01am on 30 March 2022 and will remain in place for six months.

Source: NTAA