Month in Review - February

Australian equities

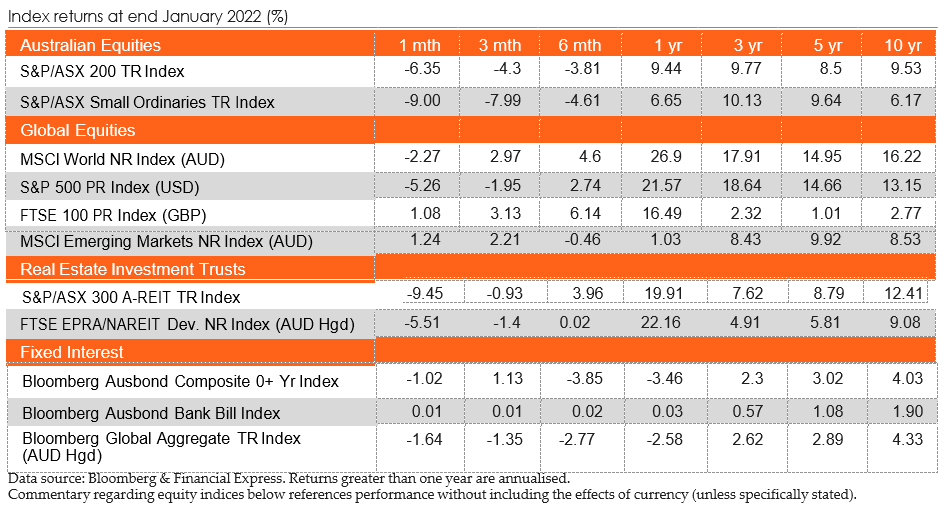

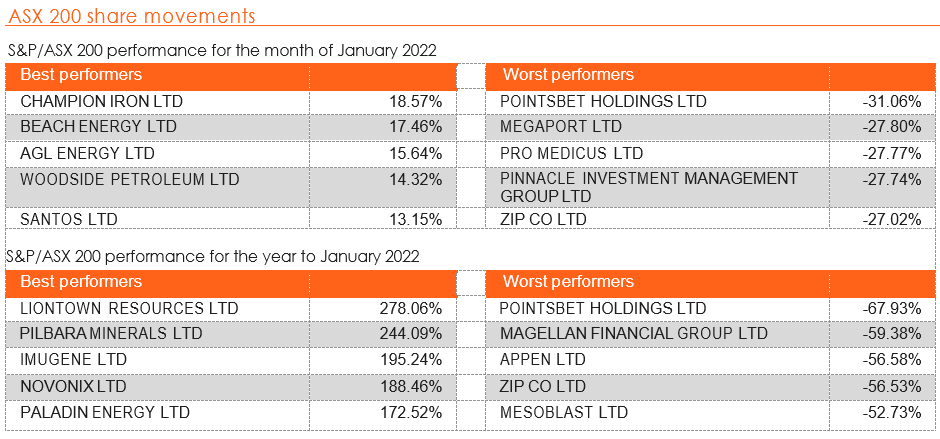

The Australian share market closed out January 2022 with the S&P/ASX 200 losing -6.4% with eight out of the eleven sectors within the Index finishing lower. Specifically, Energy was the standout sector with a return of +7.9%, whilst Utilities (+2.6%) and Materials (+0.8%) also finished positive. A heavy decline in the Information Technology sector (-18.4%) and Health Care sector (-12.1%) led what was a dismal month for the broader market.

The Energy sector was boosted by surging prices and a bullish outlook for Brent and Crude Oil in light of various tailwinds for the sector such as tight supply, geopolitical tensions and reduced fear around future lockdowns. Once again, the Information Technology sector suffered substantial losses as investors rotated from growth stocks. The catalysts included rising rates along the yield curve and several central banks indicating forward guidance of tightening monetary policy and quantitative easing to combat inflationary pressures.

Growth and Equal Weight led the decline amongst factors for the month with losses of -8.4% and -7.9% respectively. All factors finished with negative returns with growth providing the largest fall. Over the past 12 months, value is the leading factor (+14.2%), with Equal Weight (-5.7%) delivering the lowest 3-month returns.

Global equities

Subsequent to a positive end to 2021, global markets struggled in the first month of the year, challenged primarily by prospective interest rate hikes and geopolitical tensions in Ukraine.

As the AUD fell over the month of January, all of the following figures are in local currency terms for relative comparability. Developed markets slumped over the month of January declining by -4.9%, Global small caps continued to lag their broad cap counterparts posting a - 7.0% loss for the month. Emerging and Asian markets fared somewhat better with monthly returns of -1.8% and -3.8% respectively.

The key focus for investors worldwide continues to be the impact that inflation will have on markets. This has seemingly created favourable market conditions for value stocks over the last month, with value displaying monthly outperformance of over 7.4% relative to growth according to the respective MSCI ACWI Value and Growth indices in local currency terms. This is only the second time since the inception of the index that Value has outperformed growth in excess of 5%.

Property

The S&P/ASX 200 A-REIT Index (AUD) started off the year with a material drawdown, finishing the first month of 2022 down -9.5%. Global real estate equities (represented by the FTSE EPRA/NAREIT Developed Ex Australia Index (AUD Hedged)) also had a poor month, closing -5.4% lower in January. The sell-off likely stemmed from the growing concern of the Omicron variant and a hawkish Federal Reserve.

M&A activity was quieter during January across the ASX200 A-REIT sector. Centuria Capital Group (ASX: CNI) announced it has secured, off-market, the West Village in Brisbane, for $202 million, as part of an existing institutional mandate on behalf of an international sovereign wealth fund. Centuria Industrial REIT (ASX: CIP) announced a portfolio acquisition of six high-quality industrial assets across the eastern seaboard of Australia totalling $132m in value.

Despite the volatility in financial markets during January, the Australian domestic housing market advanced, with all CoreLogic reported cities experiencing positive growth during the month. Brisbane led the charge, advancing 2.3% in January. Brisbane (incl Gold Coast) is on top for YoY returns, up 30.1%, closely followed by Brisbane with 29.2%. The CoreLogic 5 capital city aggregate rose by 0.8% in January.

Fixed income

Fixed Income markets performed poorly throughout January, as concerns surrounding high rates of inflation and tight labour markets resulted in increasing yields. The Reserve Bank of Australia recently announced an end to their quantitative easing program on 10 February, but Governor Phillip Lowe has not given any indication of an increase to the cash rate in the short term, with the Board wanting to see inflation sustainably within their 2-3% target range, and increased wage growth first. Despite these statements, markets are currently pricing in 3-4 rate hikes before the end of 2022.

Over the course of January, yields for 10-year Australian Government Bonds increased by more than 20bps. This was the primary driver behind the Bloomberg AusBond Composite 0+ Year Index’s performance of -1.0% throughout January. Credit spreads also widened over the course of the month, further contributing to the Index’s poor performance.

Internationally, the US has been facing high levels of both inflation and wage growth, which has driven the Federal Reserve to adopt a more hawkish stance. While there has been no rate hike yet, the Federal Reserve’s forward guidance suggests that an increase will occur within the next few months, which is in-line with current market expectations. This, among other events, resulted in the Bloomberg Barclays Global Aggregate Index (AUD Hedged) returning -1.6% over the course of January, with currency fluctuations resulting in the unhedged variant returning 1.1%.

Economic News

Australia

The RBA left the cash rate unchanged at 0.1%, as widely expected, and decided to stop the A$275 billion bond- buying program with the final purchases to take place on February 10. The board emphasized that the halt in quantitative easing did not imply a near-term hike in interest rates as it was still prepared to be patient.

Retail sales decreased 4.40% in December, in line with expectations. The unemployment rate in December was 4.2%, 40bps lower than expected and lower than the 4.6% the previous month.

The Westpac consumer sentiment index declined 2% to 102.2 in January, with consumers in NSW and VIC appearing less unsettled by the rapid spread of the Omicron variant than those in states experiencing their first major wave of COVID infections.

The Markit Composite PMI fell to 46.7 in January, pointing to the first contraction in private sector activity in four months due to the latest surge in COVID infections as operations were disrupted.

Quarterly PPI increased 1.3% in December, 40bps above expectations and 20bps higher than the previous result whilst the yearly rate came in at 3.7%, 60bps above expectations and 80bps higher than the previous result.

The trade surplus dropped to $8.36 billion in December from an upwardly revised $9.76 billion in the previous month, the smallest surplus since March 2021.

Global

Global Covid-19 cases continue to rise with numbers surpassing 380 million cases and ten billion vaccine doses administered as at the end of January. COVID, especially the Omicron variant, remains a drag on activity and consumer sentiment. The IMF sharply cut global growth forecasts for 2022 to 4.4% in its January update, with higher-than-expected inflation and the Omicron variant worsening the outlook for the global economy. Escalating tension between Russia and Ukraine has put increased pressure on already high global energy costs.

In the US, the Federal Reserve kept its policy rate unchanged at 0.00-0.25% at its January meeting and announced that with inflation well above 2% and a strong labour market, it expects it will soon be appropriate to raise the target range for the federal funds rate.

The annual inflation rate accelerated to 7% in December, a fresh high since June 1982, but line with market expectations. Consumer sentiment dropped to 67.2 in January (68.8 expected), the lowest level since November 2011, with COVID concerns largely driving this fall.

Non-farm payrolls rose 199,000 in December, well below expectations of 4000,000, whilst the unemployment rate fell 30bps to 3.9% coming in below expectations of 4.1%. Personal incomes increased 0.4% in November, which was in line with expectations.

Non-farm payrolls rose 467,000 in January, well ahead of the market forecasts of 150,000, whilst the unemployment rate increased 10bps to 4.0% (3.9% expected). December saw personal income increase 0.3%, which is above the expected 0.4%.

PPI increased 0.2% in December, below expectations of 0.4%, with the annual rate at 9.7%.

The Markit Composite PMI slumped to 50.8 in January, signalling the slowest pace of expansion in business activity since July 2020. The Philadelphia Fed Manufacturing Index increased from 15.4 to 23.2 in January, above the expected 20.0.

The trade deficit came in at US$80.7 billion deficit in December, a slight increase on the revised US$79.3 billion deficit in November and below the expected US$83.0 billion.

The European Central Bank made no change to interest rates at its January meeting, holding them at 0.0%, and pledged to reduce its bond purchases this year despite the record rise in inflation.

The inflation rate increased 0.5% in December, with the annual rate staying at 5.2%. Economic sentiment for January was 112.7, 1.1pts lower than in December, with industrial sentiment dropping 0.7 pts to 13.9.

Retail sales fell 3.0% in December, the biggest decline in 8 months and far below the expected 0.5% increase. Annual retail sales came in at 2%, well below the expected 5.1%.

The unemployment rate fell 10bps to 7.0% in December, which was slightly below market expectations of 7.1%.

The Markit Composite PMI dropped to 52.3 in January, signalling the continued slowdown in the private sector as COVID-19 constrained activity.

PPI rose 2.9% in December, slightly above expectations of 2.8%, while the annual rate increased 26.2% (26.1% expected).

In the UK, the base interest rate remained at 0.25%, with an increase to 0.5% likely in February amid growing concern over the pressure on households from high inflation.

GDP increased 0.9% in November, ahead of the 0.4% rise expected, with the annual rate rising from 5.1% to 8.0%. Inflation rose 0.5% in December, above the expected 0.3%, taking the annual rate to 5.4%, above the expected 5.2%.

The November unemployment rate came in at 4.1%, the lowest rate since June 2020 and below market expectations of 4.2%.