Month in Review - February 2021

Australian Equities

Australian shares outperformed their global peers in January, starting 2021 with a modest gain of 0.3%. Australian equities remain largely influenced by macro factors surrounding the management of Covid-19, but the start of earnings season will see a renewed focus on fundamentals. A rotation out of some expensive growth pockets into value sectors was evident over the December quarter and into the new year, driven by vaccine developments and additional stimulus, while a significant jump in the iron ore price was the principal catalyst for a re-rating of the three largest local miners BHP, Fortescue and Rio Tinto. JB Hi-Fi released its 1H21 results, which showed an increase in sales of 23.7% on 1H20. The strong result was driven by the continued elevated customer demand for consumer electronics and home appliance products, as well as the exceptional growth in online sales, up 161.7% to $679 million. BlueScope Steel is expecting 1H21 EBIT of approximately $530 million, exceeding previous guidance of $475 million. Australian Steel Products has delivered its strongest domestic mill sales volume in a decade, while Building Products Asia & North America delivered a preliminary result approximately double that of 2H20.

Global Equities

Global shares were down over January as vaccine rollouts hit logistical roadblocks in the US and Europe, while the emergence of new viral strains of Covid-19 put a dampener on sentiment. With valuations stretched, some form of correction was to be expected, but stocks remain buoyed by the economic recovery. Since reaching their March 2020 low, the rebound in global equities has been largely led by large cap growth companies, however their beaten down cyclical counterparts experienced a pronounced recovery in the December quarter. Growth companies have been supported by persistently low interest rates, while value companies have benefitted from positive vaccine news and the reopening of economies. The US S&P 500 Index traded down through January before moving to fresh all-time highs in early February. Microsoft’s December quarter results beat estimates, revealing strong performance from Personal Computing, driven by home office and schooling needs. Alphabet (Google) also surpassed expectations, lifting revenue by 23% on the prior corresponding period, boosted by YouTube advertising, which delivered a 46% jump in revenue. Asian markets were a bright spot in January, with Japan’s Nikkei 225 Index rising 0.8%, China’s CSI 300 Index gaining 2.7% and Hong Kong’s Hang Seng Index up 3.9%.

Property

Australian listed property had a rough start to 2021, falling 4.1% in January as reports of new Covid-19 cases emerged and a drawn-out return to ‘normal’ appeared more likely. As the vaccine rollout progresses and lockdown restrictions ease, sold-off sectors such as retail may continue to strengthen and close the valuation gap with in-favour sectors such as industrial and specialised. Non-discretionary retail centres anchored by the big supermarkets and large format stores (such as Bunnings and JB Hi-Fi) have proved resilient, but discretionary mall valuations have come under pressure as owners renegotiate rents or offer better incentives to tenants. With the JobKeeper scheme set to expire at the end of March, it is anticipated that the government’s code of conduct for commercial tenancies may also cease at that time, presenting some uncertainty for SMEs in the short term. The December housing report highlighted the strength of Australia’s residential market, with turnover, prices, financing activity and dwelling approvals all posting strong gains. However, while vaccine announcements are positive for sentiment, until there is a widespread vaccine rollout, migration numbers (and commensurate population growth) will remain subdued and significantly below the levels of previous years.

Fixed Income

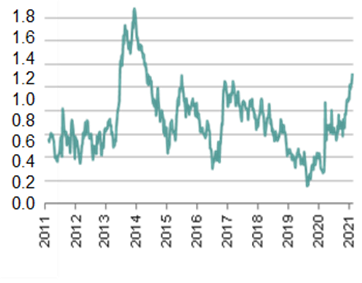

Australia’s yield curve has seen a notable steepening in recent months. Rates at the short end of the curve are being held down by the RBA, while longer-term rates are rising as optimism surrounding vaccine developments builds and inflation expectations rise. At its February meeting the RBA left the official cash rate at 0.1% but expanded its bond purchase program—due to finish in mid-April—announcing it will purchase an additional $100 billion of bonds issued by the federal and state governments. Other unconventional monetary policy measures, namely yield control on 3-year Treasuries and the Term Funding Facility, remain unchanged. The US yield curve, as measured by the spread between the 10-year and 2-year government bond yields, reached its steepest level since late 2017, with Biden’s win paving the way for more fiscal stimulus. There are fears that inflation could return to markets as the pandemic subsides and large-scale stimulus washes through the economy, however current inflation rates are still low. In Australia, the CPI increased by just 0.9% over the year to the December quarter and wages are rising at the slowest rate on record. In the US, the core PCE inflation rate (the Federal Reserve’s preferred inflation measure) was 1.5% year-on-year to December.

Economic News

Australia

New positive Covid-19 cases in New South Wales and Victoria have prompted increased testing and tracing to prevent further outbreaks. As Australia prepares for its vaccine rollout, the federal government reaffirmed its confidence in the AstraZeneca vaccine. Oxford University said work was underway to develop a new generation of vaccines that will protect against emerging variants of the virus. Meanwhile Australia’s recovery continues and has been most evident in the labour market.

The unemployment rate fell from 6.8% to 6.6% in December, lower than the 6.7% expected, as the recovery in the labour market continued to outperform expectations. 50,000 jobs were added over the month, following the strong 90,000 increase in November, while the participation rate rose from 66.1% to 66.2%. Retail sales fell 4.1% in December and were weaker than expectations of a 2.5% decline as shoppers pulled back in the crucial lead-up to Christmas, resulting in declines across five of the six retail industries. Australia’s trade balance rebounded in December to a surplus of $6.8 billion but fell short of expectations of $7.7 billion.

Australia’s manufacturing sector continues to expand, with the AiG Manufacturing PMI for the combined months of January and December rising 3.2 points to 55.3. Manufacturers reported stronger and more broad-based recovery over the summer holiday period. The Markit flash manufacturing PMI showed a 1.5-point rise to 57.2 in January, with goods producers enjoying the fastest expansions in both sales and production in over three years.

Sentiment remains strong with the Westpac-MI Consumer Sentiment Index lifting to 109.1 in February from 107.0 in January. With the JobKeeper program set to be phased out at the end of March, the ability of consumers to look ahead with confidence is critical. The ‘time to buy a dwelling’ index fell 3.1% and is now 8.6% below its peak in November. The decline in recent months suggests that increases in house prices may already be starting to weigh on the purchasing sentiment.

Global

The pandemic still looms large across the global economic landscape, with over 100 million confirmed Covid-19 cases worldwide at the start of February. The gradual rollout of vaccines is offering hope that a new normal can be achieved despite early logistical roadblocks and shortages in some regions. The Covid-19 situation in the US is improving while Europe is bringing new outbreaks under control.

In the US congress is negotiating President Biden’s proposed US$1.9 trillion stimulus package, which includes US$1,400 payments to low-income workers. Covid-19 vaccines have begun rolling out across the country as daily confirmed cases continue to fall. President Biden issued new executive orders to accelerate the production of vaccines and protective equipment, establish a Covid-19 testing board, and mandate mask wearing on public transport. US December quarter GDP rose 4.0%, in line with expectations, building on the large 33.4% rebound in the September quarter.

Despite pulling back from 60.5 in December, the ISM manufacturing PMI was robust at 58.7 in January and marked the eighth consecutive month of growth. The drop in the index was led by a slowdown in new orders, production, and new export orders. Durable goods orders rose 0.2% in December, missing expectations of 0.9% growth.

The US labour market is showing signs of weakness, with non-farm payrolls disappointing in January, gaining only 49,000 versus expectations of 105,000. The unemployment rate fell to 6.3%, well below the 6.7% expected, while average hourly earnings lifted 0.2% for the month. New home sales rose 1.6% in December, missing expectations of 1.9%. Housing starts surprised to the upside in December, coming in at a 1.67 million rate, well above the expected 1.56 million. At its January meeting the Federal Reserve made no changes to its policy settings but noted that the pace of recovery has moderated in recent months.

Australian government bond spreads are widening

*Spread between 10-yr and 2-yr AGB yields

The European Union imposed tougher restrictions on visitors from outside the bloc, with travellers from countries with a higher infection rate than the EU (more than 25 Covid-19 cases per 100,000 people over 14 days) required to enter quarantine. In the UK, home secretary Priti Patel outlined new rules for tighter border controls amid unprecedented pressure on the UK health service.

Eurozone December quarter GDP contracted 0.7% (versus -1.0% expected) following a downwardly revised 12.4% growth rate in the September quarter. The contraction was largely due to Covid-19 restrictions, with major economies Italy and France contracting 3.0% and 1.3% respectively. January’s Markit Manufacturing PMI printed in line with expectations at 54.8 but slipped back from 58.3 in December as new orders dropped.

As expected, the European Central Bank kept its key rate unchanged at zero at its January meeting, while the Bank of England also left its monetary policy settings unchanged, holding the repo rate at 0.1% and total QE purchases at £875 billion. Policymakers are still forecasting the economy to recover quickly to pre- pandemic levels as the vaccination program leads to an unwinding of Covid-19 restrictions, however the Bank of England added that banks should prepare for the possibility of negative interest rates.

China has been among the frontrunners in the global vaccine race, with late-stage trials underway for the Sinovac-developed CoronaVac in at least 16 countries across Asia, Africa and Latin America. China is making hundreds of millions of doses available to low-and middle-income countries as part of its vaccine diplomacy push. With the new Biden administration installed, the US state department said it can “walk and chew gum” when it comes to fostering a more constructive relationship while also holding China accountable for human rights abuses and sustaining America’s military and technology advantage.

On the data front it appears China’s economic recovery has hit a rough patch. The Caixin Manufacturing PMI fell to a seven-month low in January at 51.5, down from 53.0 in December and missing expectations of 52.7. Both output and new orders rose at softer paces, while export sales fell for the first time in six months due to the resurgence of Covid-19 infections globally.

Japan’s economy, which was battling recession even before the pandemic hit, remains in precarious shape. According to the IMF, Japan’s GDP is expected to grow by 2.3% in 2021 following an estimated fall of 5.3% over 2020, but much depends on how the pandemic plays out. Amid a spike in new Covid-19 cases, the Japanese government extended its state of emergency in 10 prefectures including Tokyo and Osaka and is urging companies to cut the number of workers in their offices by 70%. Japan’s unemployment rate came in at 2.9% in December, unchanged from November’s downwardly revised rate and below expectations of 3.0%.

Commodities

As the coronavirus loosens its grip on the global economy, oil demand is likely to rise. In short, the oil market has come a long way since prices turned negative during the height of the pandemic. At the same time, artificial supply constraints imposed by OPEC+ will provide additional support to prices. Brent and WTI crude prices both gained in January, ending the month at US$55.25 per barrel and US$52.16 per barrel respectively.

Base metals were mostly stronger in January, with gains in Tin (+12.1%), Nickel (+6.5%), Lead (+1.5%) and Copper (+1.2%) and falls in Zinc (-6.2%) and Aluminium (-0.1%). Gold fell 2.5% to end the month at US$1,847.65 per ounce.

Currencies

The Australian dollar was weaker in January, falling 0.7% against the US dollar to end the month at USD 0.76, but has been rising consistently since the depths of the pandemic, thanks to a weaker US dollar and rising commodity prices. The RBA’s bond purchases have helped to lower interest rates and ensure the dollar is lower than it otherwise would be.