Super re-contribution strategy explained

The tax-free super component generally consists of non-concessional contributions. Whereas, the taxable (taxed element) component is usually the remaining balance, consisting of concessional contributions* and investment earnings.

*For example, employer Super Guarantee (SG) contributions, salary sacrifice contributions, and personal deductible contributions.

When considering the receipt of concessional contributions (e.g. employer SG contributions) and investment returns over your working life, you may find your super benefits may mostly comprise of a taxable (taxed element) component.

Importantly, this fact may need to be considered from an estate planning and taxation perspective, especially, for example, where the nominated beneficiary of your super death benefit is a non-dependant for tax purposes.

When a non-tax dependant is paid a lump sum super death benefit, any tax-free component is tax-free, but the taxable (taxed element) component is taxed at 15% plus Medicare Levy. And, any taxable (untaxed element) component is taxed at 30% plus Medicare Levy.

Whereas, if a tax dependant, the super death benefit received is entirely tax-free. A tax dependant includes:

your spouse, including de-facto of the same or opposite sex

your children (including step-children) under age 18

a financial dependant

a person in an interdependency relationship with you.

Below is an overview of a strategy that can help increase the tax-free component. However, this strategy isn’t limited to super death benefits, which is also covered briefly below.

Re-contribution strategy

Overview

A re-contribution strategy generally involves the withdrawal of a portion of your super benefits as a lump sum and then re-contributing the withdrawn amount back into super as a non-concessional contribution.

On these points, it’s important to note several things:

1. To make a lump sum withdrawal, you must first meet a condition of release. For example:

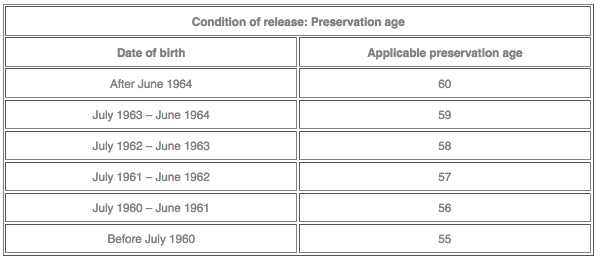

a. permanent retirement after reaching preservation age (see below table)

b. termination of a gainful employment arrangement after reaching age 60

c. reaching age 65

2. When making a lump sum withdrawal from a taxed super fund, the withdrawn amount must come proportionately from the tax-free and taxable (taxed element) component.

For example, suppose your super benefits comprise of a 10% tax-free component and a 90% taxable (taxed element) component. In that case, the withdrawn amount must have this same composition.

3. In making a lump sum withdrawal, tax may be payable. For example, while no tax is payable on the tax-free component, tax may be payable on the taxable component (see below table). If you are below age 60, it’s also important to note the withdrawal may, for example, reduce your Government co-contribution entitlement or increase your Division 293 tax or HELP debt repayments.

*2020-21 low rate cap. The low rate cap amount is indexed annually in line with AWOTE.

4. To make a non-concessional contribution, you must first be eligible to contribute. For example:

a. If you are under age 67, non-concessional contributions can be made regardless of your employment situation (please note: the age limit was increased from 65 to 67, effective from the 2020-21 financial year).

b. If you are aged from 67 to 74*, non-concessional contributions can be made, but you must first satisfy the work test^. The work test is defined as having been gainfully employed for at least 40 hours in a period of not more than 30 consecutive days in the relevant financial year.

*Non-concessional contributions may be accepted if received within 28 days of end of month in which you turn 75.

^In the first year that you don’t meet the work test, there can be an exemption from the work test, if you are aged from 67 to 74 and have a total super balance below $300,000 (on 30 June of the previous financial year). For more information, please click here.

c. Whereas, if you are aged 75 and over, non-concessional contributions can’t be made.

5. When making a non-concessional contribution, you must consider the non-concessional contribution rules. For example:

a. If you are under age 65, a maximum limit of $100,000 per financial year or up to $300,000 (known as the 'bring-forward rule') applies for non-concessional contributions. No non-concessional contributions are permitted if your total super balance exceeds $1.6 million (on 30 June of the previous financial year), and the bring-forward cap and related period phases out from $1.4 million.

b. Whereas, if you are 65 or older at all times in the financial year, the bring-forward rule isn't available and you are limited to $100,000 per year for non-concessional contributions (subject to the $1.6 million total super balance outlined above) as long as you meet the work test or the work test exemption applies.

Potential benefits (simplistic example)

With the above in mind, here is a simplistic example of a re-contribution strategy, and the potential outcomes.

John is aged 60 and retired, and has a total super balance of $500,000, comprising of a $50,000 tax-free component and a $450,000 taxable (taxed element) component.

He makes a tax-free $300,000 withdrawal from his accumulation account, comprising of a $30,000 tax-free component and a $270,000 taxable (taxed element) component.

Following this, he then re-contributes this withdrawn amount back into super as a non-concessional contribution, using the bring-forward rule. Importantly, by doing so, the following occurs:

He again has a total super balance of $500,000. However, he has now increased the tax-free component of his super benefits from $50,000 to $320,000—an increase of $270,000.

He has decreased the potential tax payable (excluding Medicare Levy) for the nominated beneficiary of his super death benefit (a non-tax dependant) from $67,500 to $27,000—a decrease of $40,500.

Other important considerations

If you are under age 65, the re-contributed amount will be preserved (i.e. unable to access) until a relevant condition of release is met (e.g. permanent retirement after reaching preservation age).

Another potential benefit of a re-contribution strategy can be the following: An increased tax-free component in super, when converted to a retirement income stream, can decrease the tax payable while you are under age 60 as the tax-free portion of pension income is not subject to tax.

With the introduction of the $1.6 million transfer balance cap limiting how much can be held in a pension account, a re-contribution strategy may be useful for transferring funds between yourself and your spouse where one of you is close to exceeding the $1.6 million threshold.

If you have any questions regarding this article, please contact us.